Travel merchant accounts are specialized payment processing solutions designed for airlines, travel agencies, tour operators, hotels, and other travel businesses that handle high transaction volumes, advance bookings, and elevated chargeback risk.

Unlike standard merchant accounts, these accounts include built-in tools to manage the unique financial complexities of the travel industry.

Running a travel business in the United States is thrilling until payment processing becomes a wall between you and your customers. A booking gets flagged.

A chargeback arrives months after a trip has ended. A payment processor drops your account without warning because “travel” sits in a high-risk category. Sound familiar?

For travel entrepreneurs, tour operators, hotel owners, and online travel agencies (OTAs), payment processing is not just a back-office task. It is the financial backbone of every reservation, package sale, and last-minute flight booking.

That is why travel merchant accounts exist. They are purpose-built for an industry where customers pay weeks or months before they ever board a plane, where chargebacks can spike during global disruptions, and where fraud risk runs higher than in most retail sectors.

This guide breaks down everything U.S.-based travel businesses need to know from how these accounts work and what they cost, to how to choose the right provider, avoid costly mistakes, and protect revenue from chargebacks and fraud. If you are launching a boutique travel agency or scaling a multi-channel tour company, this is the practical roadmap you need.

What Is a Travel Merchant Account?

A travel merchant account is a type of business bank account that allows travel companies to accept credit and debit card payments from customers. It acts as an intermediary between the customer’s payment and the business’s bank account. Standard merchant accounts rarely accommodate the travel industry’s unique risk profile, so specialized providers have developed accounts with features like delayed settlement, higher chargeback tolerance thresholds, and fraud screening tools tailored to advance bookings.

The travel industry sits in what payment processors call the “high-risk” category. This label does not mean the business is doing anything wrong. It simply reflects that travel transactions carry a higher statistical likelihood of chargebacks, cancellations, and fraud compared to, say, a hardware store. Payment processors factor this in when underwriting accounts.

Key characteristics of travel merchant accounts include:

- Acceptance of deferred or future-dated transactions

- Higher chargeback ratio tolerance (often up to 2%, vs. 1% for standard accounts)

- Rolling reserves to protect processors against sudden loss exposure

- Integration with Global Distribution Systems (GDS) like Sabre, Amadeus, and Travelport

- Support for multi-currency processing

Why Travel Businesses Are Classified as High-Risk

Travel businesses earn the high-risk label for specific, well-documented reasons and understanding them helps you negotiate better terms and set up smarter safeguards.

Advance payments and delayed service delivery sit at the heart of the problem. When a customer books a cruise six months out, the payment clears today but the service delivers half a year later. If anything goes wrong a cancellation, an airline going bankrupt, a natural disaster the customer can dispute the charge long after the payment has settled.

High average transaction values also raise processor risk. A family vacation package or a corporate travel booking can easily run into thousands of dollars. One disputed transaction of that size creates significant exposure for the acquiring bank.

Seasonal volatility amplifies the issue. Travel businesses often see massive spikes around the holidays, spring break, and summer then dramatic slowdowns in the off-season. Processors interpret unpredictable volume shifts as a warning sign.

Global exposure adds another layer. International bookings, currency conversions, and cross-border fraud attempts are all more common in travel than in domestic retail.

Types of Travel Businesses That Need Specialized Merchant Accounts

Not every business that touches travel needs a specialized merchant account, but many do. Here is a breakdown of who typically needs one and why.

| Business Type | Why Specialized Processing Is Needed |

| Online Travel Agencies (OTAs) | High volume, multi-supplier transactions, chargeback exposure |

| Tour Operators | Advance bookings, partial refunds, multi-leg itineraries |

| Hotels and Resorts | No-show disputes, deposit processing, loyalty program billing |

| Airlines (charter/regional) | Regulatory complexity, high ticket values, cancellation policies |

| Cruise Lines | Extremely high ticket values, long booking windows |

| Vacation Rental Companies | Security deposit handling, damage claim disputes |

| Travel Insurance Providers | Subscription billing, claim-related disputes |

| Corporate Travel Management | B2B payments, expense reporting integration |

If your business falls into any of these categories, a standard account from a general processor like Square or Stripe may not adequately serve your needs and may result in account termination if chargeback ratios rise.

How Travel Merchant Accounts Work

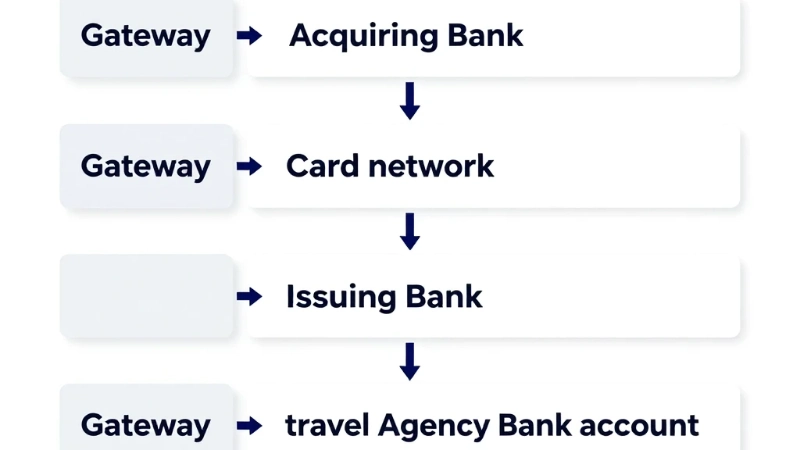

When a customer pays for a trip, the transaction flows through a chain of financial entities before the money lands in the travel business’s account. Understanding this chain helps operators spot where fees occur and where disputes get resolved.

The customer’s card information goes to the payment gateway, which encrypts and transmits it to the acquiring bank (the merchant’s bank). The acquiring bank routes the transaction through the card network (Visa, Mastercard, American Express) to the issuing bank (the customer’s bank). The issuing bank approves or declines the transaction, and the response travels back through the same chain in seconds.

For travel businesses, this process includes a few extra layers. Most travel merchant accounts operate with a rolling reserve, where the processor holds back a percentage of each transaction typically 5 to 10 percent for a period of 90 to 180 days. This reserve acts as a buffer against potential chargebacks or refunds. Once the reserve period passes without a dispute, the funds release to the merchant.

The settlement timeline also differs from standard retail. While a standard merchant account might settle funds within one to two business days, travel accounts sometimes operate on extended settlement schedules that align with when the service is actually delivered.

Key Features to Look for in a Travel Merchant Account

Choosing the right travel merchant account means matching features to your specific business model. Not all providers offer the same toolkit.

Payment gateway compatibility matters enormously. Your gateway needs to integrate with your booking engine, GDS system, property management system (PMS), or tour management software. Poorly matched integrations create friction at checkout and increase cart abandonment.

Chargeback management tools are non-negotiable. Look for providers that offer real-time chargeback alerts through networks like Verifi (owned by Visa) or Ethoca (owned by Mastercard). These alert systems notify you of a dispute before it officially becomes a chargeback, giving you time to resolve it directly with the customer and avoid the financial penalty.

Fraud screening and 3D Secure 2.0 (3DS2) authentication reduce unauthorized transaction claims. 3DS2 adds a verification step for online payments without creating excessive friction for legitimate buyers.

Multi-currency support opens your business to international travelers. Look for dynamic currency conversion (DCC) and competitive foreign exchange rates built into the processing agreement.

Recurring billing capability matters if you sell travel subscriptions, membership programs, or installment payment plans for expensive packages.

Understanding Chargeback Risk in the Travel Industry

Chargebacks are the single biggest financial threat to travel merchant accounts. A chargeback occurs when a customer contacts their bank to dispute a charge rather than working directly with the merchant. The bank pulls the funds back, adds a chargeback fee (usually $20 to $100 per incident), and opens a dispute process.

For travel businesses, chargebacks spike for predictable reasons: customers disputing charges after trip cancellations, not recognizing a descriptor on their statement, or committing friendly fraud (claiming a service was never delivered when it was).

Card networks set a chargeback ratio threshold of 1 percent of total monthly transactions for standard merchants. High-risk processors extend this to around 2 percent before imposing penalties. Exceeding this threshold can trigger account suspension or termination and being placed on the MATCH list (Member Alert to Control High-Risk Merchants) can make it extremely difficult to obtain processing elsewhere for up to five years.

Three proven strategies to reduce chargebacks:

- Use clear, recognizable billing descriptors that match your business name exactly as customers know it.

- Send detailed confirmation emails with cancellation policies spelled out in plain language before the trip date.

- Enroll in Visa’s and Mastercard’s chargeback alert programs to resolve disputes before they escalate.

Rolling Reserves: What They Are and How to Negotiate Them

Rolling reserves are one of the most misunderstood aspects of travel merchant accounts. Many new operators see a reserve requirement as a red flag, but it is actually a standard underwriting practice in high-risk processing.

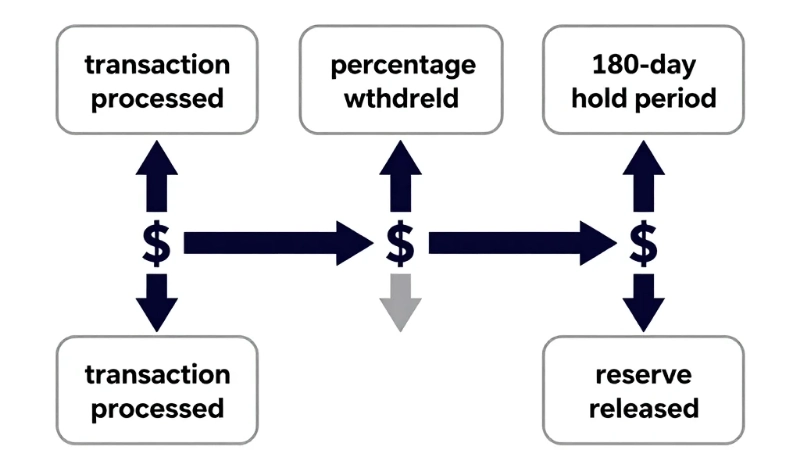

A rolling reserve works like this: the processor withholds a fixed percentage of each transaction commonly 5 to 10 percent and holds it for a defined period, usually 90 to 180 days. At the end of that period, the oldest reserves release on a rolling basis, creating a continuous cycle of holdbacks and releases.

For a travel business processing $50,000 per month at a 10 percent reserve, that means $5,000 is withheld each month. After six months, releases begin matching the withholds, and cash flow stabilizes.

Insider tip: As your chargeback ratio improves and your processing history lengthens, you can renegotiate reserve terms. Most processors will reduce the reserve percentage or shorten the hold period after six to twelve months of clean processing history. Always ask for a reserve review clause written into your contract.

Alternatives to rolling reserves include upfront reserves (a lump-sum deposit held in escrow) and capped reserves (a maximum dollar amount rather than an ongoing percentage). Depending on your cash flow situation, a capped reserve may serve you better even if the initial deposit feels steep.

Fees Associated with Travel Merchant Accounts

Travel merchant account fees run higher than standard accounts because of the elevated risk profile. Knowing what each fee covers helps you compare providers accurately.

| Fee Type | Typical Range | What It Covers |

| Discount Rate (per transaction) | 2.5% – 4.5% | Interchange + processor margin |

| Monthly Account Fee | $25 – $100 | Account maintenance |

| Chargeback Fee | $20 – $100 per incident | Dispute processing |

| Rolling Reserve Holdback | 5% – 10% per transaction | Processor risk buffer |

| PCI Compliance Fee | $75 – $150/year | Security certification |

| Gateway Fee | $10 – $30/month | Payment routing infrastructure |

| Early Termination Fee | $250 – $500+ | Contract exit penalty |

Always request an interchange-plus pricing structure rather than a flat-rate or tiered model. Interchange-plus passes through the exact Visa/Mastercard interchange rate and adds a fixed processor markup, giving you full transparency and typically lower overall costs at higher volumes.

How to Apply for a Travel Merchant Account

The application process for a travel merchant account is more detailed than a standard account because underwriters need to assess your specific risk profile. Being prepared speeds up approval and improves your terms.

Documents typically required:

- Business license and entity formation documents (LLC, S-Corp, etc.)

- Three to six months of recent bank statements

- Three to six months of prior processing statements (if applicable)

- Voided business check for ACH settlement

- Government-issued ID for all owners with 25 percent or more equity

- Website URL showing clear terms of service, refund policy, and contact information

- Sample booking confirmation or invoice templates

Underwriters will review your chargeback history, business model, average ticket size, and monthly processing volume. If your business is new and lacks processing history, expect higher reserve requirements initially. Being transparent about your business model actually works in your favor processors prefer operators who understand their risk profile and demonstrate controls for managing it.

Top Payment Processors for U.S. Travel Businesses

The U.S. market includes several processors that actively serve the travel sector. Each comes with different strengths depending on business size, processing volume, and industry segment.

PaymentCloud specializes in high-risk industries including travel and has built strong relationships with multiple acquiring banks, which increases approval odds for newer or previously terminated businesses.

Durango Merchant Services works with travel companies across the spectrum, from boutique agencies to multi-channel tour operators, and offers competitive rates with flexible reserve structures.

Host Merchant Services focuses on transparent pricing and strong U.S.-based customer support, making it a solid choice for smaller travel agencies that prioritize access to real humans when problems arise.

Stripe and Square are sometimes used by micro-travel businesses, but both carry a risk of sudden account termination for high-risk categories. They work better as a secondary processor than a primary one.

Authorize.net as a gateway pairs well with various acquiring banks that specialize in travel it integrates with most major booking platforms and supports advanced fraud detection tools.

Always compare at least three processors side by side using the same hypothetical monthly volume and average transaction size. Small differences in discount rates compound significantly at scale.

Common Mistakes Travel Businesses Make with Payment Processing

Even experienced travel operators make avoidable errors that cost them money, accounts, or both.

Mistake 1: Using a general processor without disclosing the business type. Some operators sign up with Stripe or PayPal without declaring they operate in travel. When chargeback ratios rise or the processor identifies the business type during a routine review, the account gets terminated without warning. The fix is to always apply through a processor that explicitly supports travel and high-risk merchants.

Mistake 2: Ignoring the billing descriptor. A billing descriptor is the text that appears on a customer’s credit card statement. If it reads something vague like “ONL BOOKING 888-555-0100,” customers frequently fail to recognize the charge and dispute it. The fix is to set the descriptor to your recognizable brand name and add a customer service phone number.

Mistake 3: Skipping PCI DSS compliance. The Payment Card Industry Data Security Standard (PCI DSS) is not optional it is a contractual requirement for any business that accepts card payments. Non-compliance can result in fines of $5,000 to $100,000 per month and catastrophic liability in the event of a data breach. The PCI Security Standards Council (PCI SSC) at pcisecuritystandards.org publishes free self-assessment questionnaires that most small travel businesses can use to achieve compliance.

Travel Merchant Accounts and Fraud Prevention

Fraud prevention is inseparable from payment processing for travel businesses. The industry’s global reach and advance-payment model make it a prime target for card-not-present (CNP) fraud, account takeover, and synthetic identity fraud.

Address Verification Service (AVS) checks the billing address a customer provides against the address on file with their card issuer. Mismatches flag suspicious transactions before they process.

Card Verification Value (CVV) requirements prevent fraudsters who have stolen card numbers but not the physical card from completing purchases. Always require CVV at checkout.

Velocity checks flag when the same card or IP address attempts multiple transactions in a short window a common pattern in automated fraud attacks.

Device fingerprinting tools identify the device used to make a booking and compare it against known fraud patterns. Many travel-specific payment gateways include this as a standard feature.

The U.S. Federal Trade Commission (FTC) publishes updated guidance on online payment fraud at ftc.gov/business-guidance a useful resource for staying current on emerging fraud tactics targeting travel businesses.

Travel Insurance and Payment Processing: An Overlooked Connection

Travel insurance and merchant accounts interact in ways that surprise many operators. When a customer purchases travel insurance through a third-party provider bundled into a booking, the payment processing for that insurance premium may require a separate merchant account or a specific merchant category code (MCC).

More practically, offering customers access to travel insurance at checkout reduces chargebacks. When travelers know they have insurance protection for cancellation, illness, or trip interruption, they are less likely to dispute a charge with their bank if plans change. According to the U.S. Travel Insurance Association (USTIA), insured travelers file significantly fewer chargebacks than uninsured travelers on comparable bookings.

Partnering with insurance providers like Allianz Travel, Travel Guard (AIG), or World Nomads to offer embedded insurance at the point of booking serves customers better and protects your processing account simultaneously.

International Processing and Multi-Currency Considerations

U.S. travel businesses that serve international customers or book travel to international destinations frequently encounter multi-currency processing challenges. Accepting payment in a customer’s local currency improves conversion rates but introduces exchange rate risk and additional processing fees.

Dynamic Currency Conversion (DCC) lets international customers pay in their home currency at checkout. While this improves the customer experience, the exchange rate applied typically favors the processor. Build this into your pricing model if you offer DCC.

Multi-currency settlement allows your business to hold funds in multiple currencies before converting to USD, potentially reducing conversion losses during favorable exchange rate windows.

Businesses processing significant international volume should also consult with a tax advisor about foreign transaction reporting requirements under IRS guidelines and FinCEN regulations for businesses handling cross-border payments above certain thresholds.

How to Switch Travel Merchant Account Providers

Switching processors mid-operation requires careful planning to avoid payment disruption or double-reserve situations.

First, apply and receive approval from the new processor before giving notice to your current one. Never close an existing account before a replacement is fully operational. During the transition, maintain both accounts in parallel for 30 to 60 days to ensure all in-flight transactions and potential chargebacks process correctly through the original account.

Update your payment gateway settings, booking system integrations, and any saved card tokens before the cutover date. Communicate expected downtime to your team in advance, even if it is minimal.

Ask your new processor for a written commitment on reserve terms, rate locks, and the process for reserve release at the end of your relationship. These terms are negotiable upfront but nearly impossible to change after the contract is signed.

Insider Tips for Travel Merchant Account Success

After analyzing how the most successful U.S. travel businesses manage their payment processing, five practices consistently separate the operators who thrive from those who scramble.

Tip 1: Monitor your chargeback ratio weekly, not monthly. By the time your monthly statement shows a ratio problem, your account may already be flagged. Most processors provide real-time dashboards use them.

Tip 2: Write a cancellation policy that is impossible to misread. Place it in the booking flow, in the confirmation email, and on the receipt. When customers understand what they agreed to, they are far less likely to dispute a legitimate charge.

Tip 3: Match your payment processor to your booking volume, not your current volume. If you expect to grow from $30,000 to $200,000 in monthly processing within 18 months, choose a processor who can handle that growth without re-underwriting your account from scratch.

Tip 4: Keep six months of bank and processing statements organized and accessible. Processors request these regularly for account reviews, and delays in providing them can trigger temporary holds.

Tip 5: Build a direct relationship with your processor’s risk team. Knowing who to call when a chargeback spike hits rather than navigating a general support line can mean the difference between a temporary hold and a full account termination.

Frequently Asked Questions

What is a travel merchant account and who needs one?

A travel merchant account is a specialized payment processing account designed for businesses in the travel industry, including airlines, hotels, travel agencies, tour operators, and vacation rental companies. Any business that sells travel-related services especially those involving advance payments needs one to handle the higher chargeback risk and delayed settlement cycles that standard accounts cannot accommodate.

Why is the travel industry considered high-risk by payment processors?

Payment processors classify travel as high-risk because of advance payment structures (service delivered months after payment), high average transaction values, seasonal volume volatility, global fraud exposure, and historically elevated chargeback rates. These factors increase the potential financial liability for acquiring banks, which translates into stricter underwriting requirements and higher processing fees for travel businesses.

How much does a travel merchant account cost?

Costs vary by processor, volume, and business risk profile. Typical discount rates range from 2.5 to 4.5 percent per transaction, with monthly fees of $25 to $100, chargeback fees of $20 to $100 per incident, and a rolling reserve holdback of 5 to 10 percent. Interchange-plus pricing structures generally deliver lower overall costs for businesses processing more than $10,000 per month.

Can a new travel business get approved for a merchant account?

Yes, though expect stricter terms. New businesses without processing history will typically face higher reserve requirements and slightly elevated rates. Providing a strong business plan, a professional website with clear terms and refund policies, and clean personal credit history for all owners meaningfully improves approval odds. Some processors specialize in startup travel merchants.

What is a rolling reserve and when does it get released?

A rolling reserve is a percentage of each transaction typically 5 to 10 percent withheld by the processor for a set period, usually 90 to 180 days, as a risk buffer. After the hold period, reserves release on a rolling basis. With a clean chargeback history, operators can often negotiate reduced reserve terms after six to twelve months of processing.

How do I reduce chargebacks for my travel business?

Use clear billing descriptors that customers recognize, send detailed booking confirmation emails with cancellation policies, enroll in Visa’s and Mastercard’s chargeback alert programs (Verifi and Ethoca), require CVV at checkout, and offer travel insurance at the point of booking. Proactive customer communication before and during trips also significantly reduces post-trip disputes.

What happens if my travel merchant account gets terminated?

Account termination can result in placement on the MATCH list, which blocks you from obtaining merchant accounts with most processors for up to five years. Before termination reaches that stage, work proactively with your processor’s risk team to address chargeback spikes or policy violations. If termination occurs, specialized high-risk processors can sometimes provide new accounts even for MATCH-listed merchants, though terms will be significantly stricter.

Conclusion

Three things matter most when it comes to travel merchant accounts: choosing a processor built for your industry’s unique risk profile, managing chargebacks proactively before they become account-threatening, and understanding the rolling reserve structure so it does not blindside your cash flow.

Travel businesses that treat payment processing as a strategic function not just an operational one protect their revenue, their customer relationships, and their ability to scale. The right merchant account provider becomes a genuine business partner, not just a fee-charging middleman.

Start by auditing your current processing setup against the features outlined in this guide. If your existing account lacks chargeback alert integration, multi-currency support, or industry-specific fraud tools, it may be costing you more than the processing fees suggest. The U.S. travel market rewards operators who get the back-end infrastructure right because that frees them to focus on what actually matters: delivering experiences that make travelers come back.

Always verify current fees, reserve requirements, and regulatory guidelines directly with your processor and legal advisor, as rates and policies change regularly.

Ben Fogle believes that true adventure begins where the pavement ends. After spending years documenting extreme environments, rowing across oceans, and trekking through frozen landscapes, he mastered the art of wilderness travel. For Travelmarse, Ben constructs highly detailed guides on deep-nature packing lists, wildlife safety, and sustainable eco-tourism. He breaks down intimidating, rugged expeditions into clear, step-by-step roadmaps so everyday travelers can safely connect with the natural world.